Welcome back to our series on financial accounting for small businesses! In our last post, we explored analyzing financial health through comparative financial data. Today, we’re diving into the heart of accounting – recording transactions and balancing the books.

Recording Transactions: The Foundation of Financial Accounting Understanding the Accounting Equation

Every transaction in business affects its financial position, represented by the basic accounting equation: Assets = Liabilities + Equity. Understanding how each transaction impacts this equation is crucial for maintaining accurate records.

Debits and Credits: The Language of Accounting

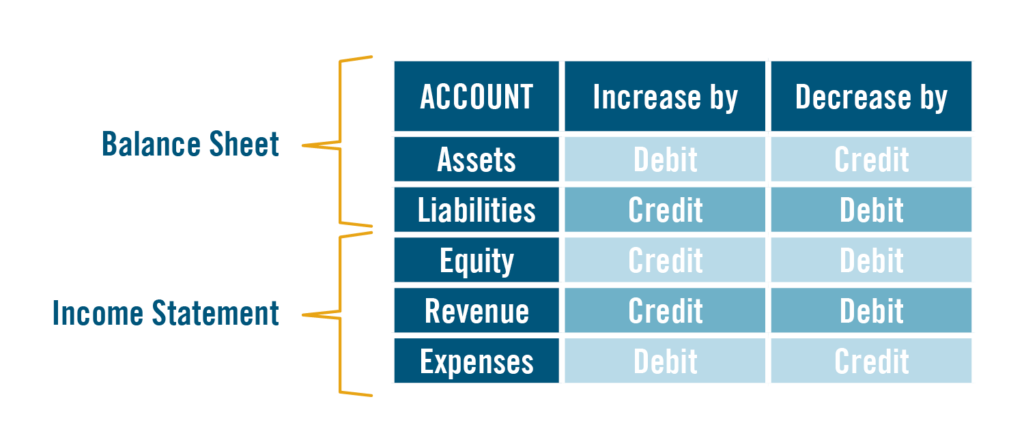

In accounting, every transaction is recorded using debits and credits. These are not just mere additions or subtractions but a systematic way to keep track of how transactions affect different accounts. This part can be particularly confusing, especially as most of us are used to looking at our bank transactions from a consumer perspective. A credit to your cash means you have more money, right? Wrong. Check out the table below for an example of the effect of debits on credits have on different accounts.

The Journal: Chronologically Capturing Transactions The Role of the Journal in Accounting

The journal, often referred to as the book of original entry, is where all transactions are recorded first, in chronological order. It’s the starting point of the accounting process.

From Journal to Ledger: Organizing Financial Data Understanding Ledgers and Posting

After recording transactions in the journal, the next step is posting them to the ledger. The ledger is a collection of all accounts a business uses, organized for ease of reference and calculation.

The Trial Balance: Ensuring Accuracy in Accounts What is a Trial Balance?

A trial balance is prepared to ensure that debits equal credits, a fundamental check for accuracy in accounting. It lists all ledger account balances at a specific point in time.

The Importance of a Balanced Trial Balance

A balanced trial balance is a sign that your accounts are correctly balanced. It’s a vital step in the accounting process, paving the way for preparing financial statements.

Conclusion

Recording transactions accurately and maintaining balanced books are the backbones of sound financial management for any small business. By mastering these skills, you set the stage for robust financial health and strategic business growth.